The PRA had repeatedly warned the bank about the “poor state of its trading controls” and the bank’s own compliance and internal risk functions flagged their unsatisfactory state on multiple occasions. A number of incidents, audits and compliance reviews, beginning in 2018, all underlined their persistent weakness and culminated in a serious equity trading incident in 2022. This has led to the imposition of a fine of £33.8m ($43.03m) by the PRA and £27.7m ($35.3m) by the FCA.

Fat finger error roils European markets

The incident took place on a Bank Holiday Monday in the UK when a trader, intending to sell a $58m basket of equities, used the wrong input field and accidentally loaded this basket with an order of $444 billion comprising 349 stocks across multiple European markets.

Although the system immediately generated 711 warning messages, these were listed in a single alert with only the first 18 lines visible to the trader (who had to scroll down in order to view the remainder).

The warning messages included two ‘hard block’ warnings, which could not be overridden. These stopped $248 billion of equities in the basket from moving to execution.

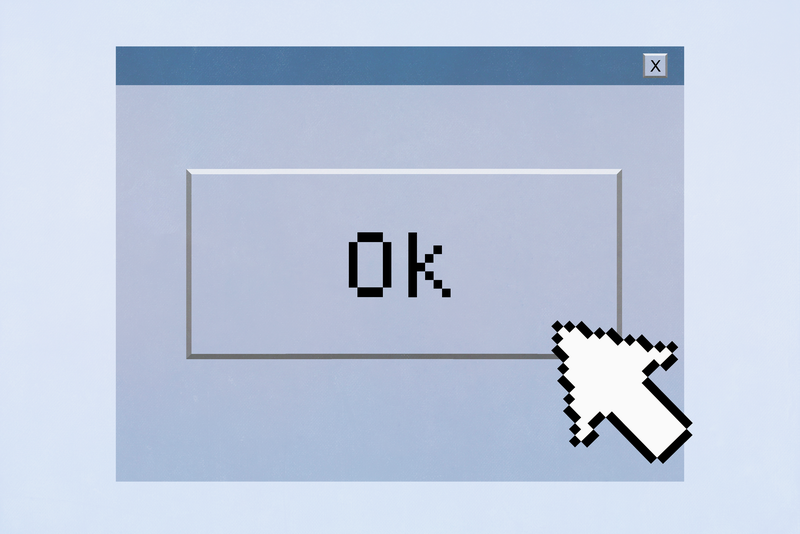

However, the trader was able to override the ‘soft block’ warnings. Then, despite being presented with a notional value (now only(!) $196 billion) of the equities in the basket in a final pop up, the trader pressed ‘OK’ and executed the remainder of the order.

Seven orders were blocked by Citi’s controls, which reduced the basket size to $189 billion. The remainder were sent to be executed, were sliced and scheduled for trading over the rest of the day.

Additional controls operated as expected while the orders were executing and reduced the basket further to $24.6 billion.

Of this, $1.4 billion sell orders were executed, which led to a drop in several European indices.

Approximately 10 minutes after hitting the OK button the trader discovered his error and “after several attempts” succeeded in cancelling the order.

Monitoring desks miss the issue

Because it was a bank holiday the bank’s algorithmic service desk responsible for the monitoring of internal executions was not staffed.

Responsibility for order monitoring was passed to the electronic execution desk, which was primarily responsible for monitoring orders originating from external clients. Staff on this desk did not escalate the alerts generated by the system.

Incoming client queries alerted staff to the unexpected drop in the European indices. But they did not connect this market activity with the alerts they had received or the order placed by the bank.

Because their system filtered out almost all of the alerts and most of the notional order value neither did the team responsible for post-trade monitoring. They did escalate the incident back to the electronic execution desk via email, 20 minutes after the order was cancelled by the trader, following up four hours later when no response was received. By this time, of course, the damage had been done, the order cancelled and the indices were all back to normal.

Lack of hard blocks and calibration issues

Both the FCA and the PRA draw attention to the fact that the erroneous trade was executed as a result of Citi’s failure to implement effective and appropriate controls, in particular hard blocks, that would have prevented or at least limited the size of the order.

These controls were lacking both at the point when the order was placed, permitting a trader to override alerts that remained unread for example, as well as at the point of execution. The controls that were in place were also poorly calibrated, which made them ineffective even in instances when they could have functioned as expected.

The regulators were also unhappy with what they deemed as an inadequate response from the desks responsible for trade monitoring, deeming their actions a missed opportunity to cancel the erroneous order and a demonstration of “serious failings” in the bank’s monitoring control framework.

Finally, the size of the fine is reflective of the fact that the bank had plenty of warning that there were problems with its trading systems and controls. It was not only the incidents, audits and reviews that should have resulted in action – better practice was already being followed internally – a hard block on the notional basket size, which could have stopped the erroneous order entirely, had been in place in a comparable trading desk in New York since 2013.