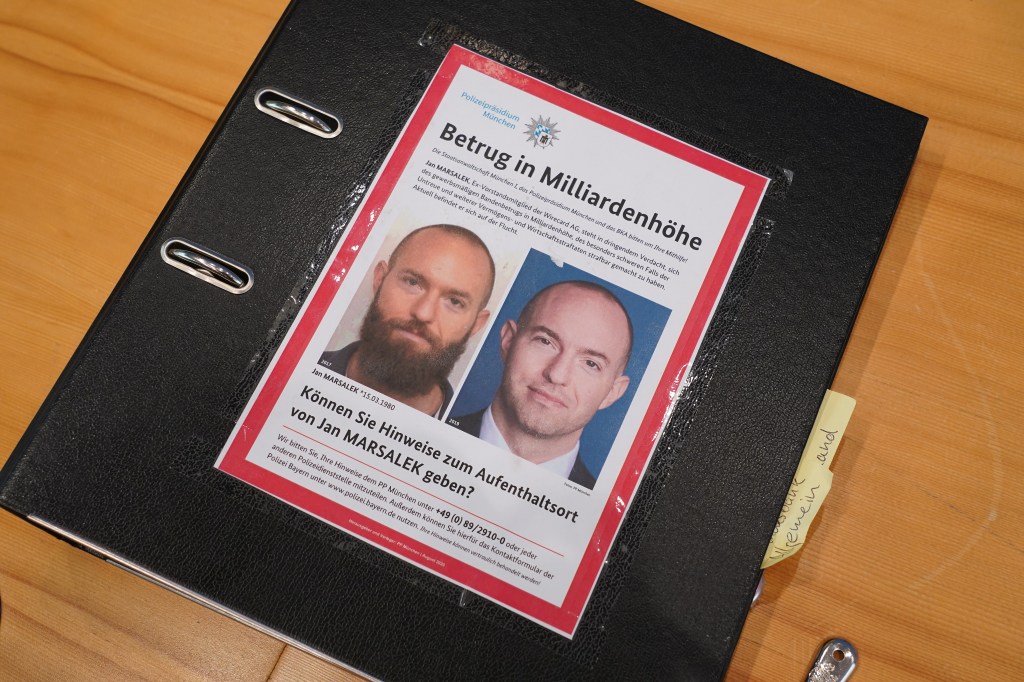

At its peak, German payments company Wirecard was worth €24bn ($25.4), more than Deutsche Bank. It was the darling of the German fintech industry — proof that German fintech startups could compete with the world’s biggest tech companies.

And then it all unraveled. In June 2020, the company was forced

The